Business

Cashless ATMs May Disappear, But You May Not Have to Bring Cash to a Dispensary After All

How can you pay for marijuana at dispensary?

My last column addressed why cashless ATMs were not legal. Today, we discuss why some payment platforms are compliant.

A writer never knows what stories will resonate with an audience or how loudly. My December column about cashless ATMs was timely, with dispensaries across the country going cash-only as the feds cracked down on less-then-legal workarounds. Still, the high rate of clicks, reposts, and responses was unexpected. One reader, a payment platform expert witness, used our story to explain to his client’s attorneys why cashless ATMs were such a problem.

Another reader asked about decoupled debit, which I have come to learn could be a workable product for cannabis businesses. Decoupled debit is different from PIN debit—it feels similar, but when you peel back the layers it is much different. I briefly touch upon the differences below …

Ghost of the BIG bankcard company

Our experts assured me that PIN debit is not legal. At its core, PIN debit involves a bank or network-issued card and those issuers do not knowingly allow cannabis over their networks. To make PIN debit work typically involves concealment, which the feds consider to be fraud. The provider might simply lump their cannabis transactions into another merchant code, such as pharmacy. That works until the banks find out, whereupon the banks will terminate the network or simply refuse to accept any pharmacy transactions. As Yogi Berra once said, “It’s like déjà vu all over again.” We could be recycling the cashless ATM article and simply changing it to PIN debit.

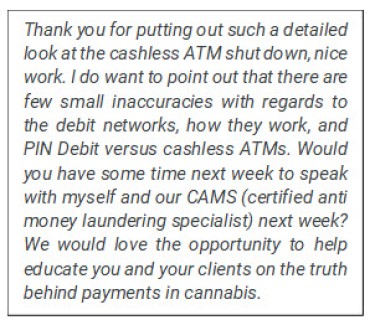

Another reader, the chief marketing officer for a PIN debit provider, explained that we did not fully understand the product. That reader said they have many clients, including a roster in Massachusetts. The CMO set up a call between me and their in-house CAMS (Certified Anti Money-laundering Specialist) expert but canceled, stating they were busy managing an influx of new clients seeking a solution when their cashless ATM terminals stopped working. Then they went silent. When they resurfaced they stated, “As part of our initiatives for 2023 we are electing to not be involved in third party publications unless we have full control of the end product.” They never detailed my “few small inaccuracies with regards to the debit networks, how they work, and PIN Debit versus cashless ATMs.” I asked for the name of a local participating retailer so we could see how the system works, but they declined to provide one.

Another reader, the chief marketing officer for a PIN debit provider, explained that we did not fully understand the product. That reader said they have many clients, including a roster in Massachusetts. The CMO set up a call between me and their in-house CAMS (Certified Anti Money-laundering Specialist) expert but canceled, stating they were busy managing an influx of new clients seeking a solution when their cashless ATM terminals stopped working. Then they went silent. When they resurfaced they stated, “As part of our initiatives for 2023 we are electing to not be involved in third party publications unless we have full control of the end product.” They never detailed my “few small inaccuracies with regards to the debit networks, how they work, and PIN Debit versus cashless ATMs.” I asked for the name of a local participating retailer so we could see how the system works, but they declined to provide one.

Needles in the trim stack

Our research and discussion with experts indicate the only workable solution, other than cash, is a platform built upon the automated clearing house, more commonly known as ACH. ACH is the engine behind many common payment applications, from Venmo, to PayPal, to Zelle. According to the Consumer Financial Protection Bureau (CFPB), the US government agency that makes sure banks, lenders, and other financial companies treat you fairly:

ACH is an electronic fund transfer made between banks and credit unions across what is called the Automated Clearing House network. ACH is used for all kinds of fund transfer transactions, including direct deposit of paychecks and monthly debits for routine payments… A number of online payment services also conduct transactions via ACH, including most banks and credit unions’ online bill payment services. While many ACH payments clear quickly, because of the way in which an ACH is processed and precautions against fraud and money laundering, transactions can sometimes take several days to complete. (To learn more about ACH, I recommend this article on nerdwallet.com)

Decoupled debit

Two seemingly credible experts provided different explanations of decoupled debit, and both seem very plausible. I’ll explain the one that seems most relevant to today’s discussion.

Decoupled debit is basically a private card network. If you’ve been in a retailer or gas station that has its own debit card (that refills itself from your bank account), you’re using a decoupled debit card. It is decoupled from the conventional debit networks (which do not allow cannabis transactions) and funds itself via ACH but can generally only be used at the sponsoring retailer’s outlets.

The experts we spoke with all confirmed that ACH is an acceptable payment method. The challenge is that ACH does not have a manner to check balances in live time (like instantaneously during a retail transaction while at the check-out station) and ACH clears after the transaction, creating an opportunity for insufficient funds and a loss to the sponsor or retailer.

I spoke with the CEOs of two legal payment platforms—Dustin Eide, the CEO of CanPay, and Cathy Iannuzzelli, the president of Kind Tap. We learned that finding payment providers is easy, finding honest payment providers is a bit more challenging, and finding compliant payment providers is especially tricky. We identified only four. We spoke with two of them for this article.

With the industry scrambling to find replacement solutions to cashless ATMs and many vendors continuing to push PIN debit or other disguised payment methods as legal, I took a dive into workable solutions. My last column addressed why cashless ATMs were not legal. Today, we discuss why some payment platforms are compliant. Because this is such a timely issue in the cannabis industry, we get down to a granulated level.

CanPay

When Colorado legalized cannabis, Dustin Eide saw an opportunity to develop a legal payment platform. He had the first ingredient we have seen in common with other legal payment platforms—experience in the payment industry. Dustin recognized the challenge and saw the opportunity. With a background in traditional merchant services, he sought to design a plan that would avoid the worst ISO (independent sales organization, the small local firms that generally sell merchant services) practices and work efficiently for consumers.

Dustin quickly understood that the card networks were being honest that they would not allow cannabis transactions. But ACH does not touch a card network. FinCEN-regulated financial organizations were transparently using ACH and maintaining compliance with FinCEN’s Valentine’s Day 2014 guidance outlining the US Treasury’s “expectations regarding marijuana-related businesses” and “marijuana laws and law enforcement priorities.” He tested various solutions with banks to find a legitimate process.

Today, CanPay has more than 1,000 participating retailers across 31 states. According to Dustin, CanPay is accepted by 10 of the 13 largest publicly traded MSOs. Unlike a private network where the solution is one card per store, CanPay acts as a universal payment tool—it is one app per network of 1,000 unrelated stores, and its value enhances as they add more participating retailers.

How it works

CanPay is a containerized site that functions like a mobile web-based app. The icon is saved to a user’s home screen and when clicked, instead of launching a native app (locally stored), it connects to the CanPay website. It takes up no space on the user’s device and functions in many regards like Microsoft Office 365, working seamlessly on the local device but residing in the cloud. The app can be used at any retail store that is registered with CanPay.

To use the service, the customer opens the app and requests a code. The participating retailer scans the code, and the transaction is complete. If the code cannot be scanned, the retailer types it into their system. The codes are single use with a 30 minute use-it or lose-it lifespan. The code has no personal or banking data. The app has a live chat with real time live agents, whether the issue is signup or a problem at the point of sale.

CanPay was designed as a low-cost provider. Account fees generally cost the merchant 2% to 2.5% of the transaction amount. Higher rates can reach 3.5% and great rates are in the 1.5% to 1.75% range. CanPay priced itself at less than 2%, all-in, with no setup or fixed monthly fees.

Over six-and-a-half years since June 2016, starting with three dispensaries in Colorado, CanPay has processed more than $700 million in retail transactions. Customers sign up for the app online in about two minutes. Signup requires a name, phone number, email, address, and date of birth. The customer links in their bank account (which requires a bank routing number and the customer’s account number—CanPay claims its app has direct links to over 11,000 financial institutions). CanPay designates a unique spending limit, up to $5,000. Once signed up, the app is live and can be used at any participating retailer.

The consumer is not required to pre-fund the transaction or keep a balance on deposit with CanPay. The service is completely free to the consumer. Dustin explained that CanPay was designed to avoid what merchants hate—long-term contracts, exclusivity, monthly fees, compliance fees, activation, and setup fees. Consumers were familiar with Venmo, ApplePay, and other payment platforms, so CanPay sought to develop a dedicated cannabis payment network functioning exclusively over the ACH network (as many payment apps do). CanPay retailers can operate in full transparency regardless of the words (like cannabis, marijuana, or their slang references) in their business’ name. CanPay has presented its platform to federal bank examiners without pushback or objections.

More than 120 financial institutions participate in the CanPay network.

ACH is not immediate and has no payment holds, but CanPay guarantees payment even if the ACH fails. If an ACH request does fail, the customer can open the app to clear the failure by depositing funds to their bank account and initiating a fresh ACH transaction. CanPay does not assess a fee if the ACH fails, though the consumer’s bank might do so. CanPay clears transactions daily.

All transactions happen within the scope of federal enforcement priorities.

KindTap

KindTap’s founding team reviewed the cannabis payment market and realized all the compliant platforms were using ACH and there were no consumer credit products. The team knew the traditional payment networks were not available, so they developed their own network.

The KindTap team understood both the payment and credit side of the equation and knew that a consumer credit product was the missing link – the ability to buy now and pay soon after. Studies have shown that when consumers use a credit device like a credit card, average spending increases.

KindTap has reviewed nearly a year of payment activity and found that KindTap Credit customers spend over 50% more than when they pay with cash and over 20% more than when they pay with a bank account linked product like ACH.

How it Works

When a merchant signs up for a KindTap account, KindTap conducts due diligence that includes confirming the merchant has a state cannabis license in good standing and has a cannabis-approved depository account with a cannabis compliant bank. KindTap adheres to the Cole memo’s eight enforcement priorities. KindTap requires its clients have cannabis compliant bank accounts to assure day to day compliance and oversight of general financial transactions. This weeds out (no pun intended) operators who do not have a cannabis-friendly depository account.

KindTap is designed to be consumer friendly. Conventional credit card requires minimum payments structured so low that it can take years to pay off a balance. KindTap requires a minimum monthly payment of 25% of the outstanding balance to avoid systemic consumer debt. KindTap underwrites consumers for a credit line from $250 to $1,500. These limits are intended to keep consumers from overspending.

KindTap rolled out its service during COVID and as a result they focused on eCommerce. Customers can order online, in advance. To allow for in-store use, participating retailers can install a KindTap kiosk that allows the customer to place an order at the store. KindTap reported that the company is presently working on strategies to allow their system to function in most store environments (like at the check-out station). KindTap integrates into the ordering process, such that payment is made when the order is placed, regardless of when the order is picked up or delivered. Monthly statements, like credit card statements, are sent by email or available in the app. The consumer then pays the bill like any other standard credit card product. There is no transaction fee or annual fee to the consumer. The only cost to the consumer is an interest charge if the balance is not paid in full each month.

For the retailer there are no fees for set-up, no monthly fees, and no minimum usage is required. A retailer can cancel at any time. There is a transaction fee each time a sale is made with KindTap. These fees are higher than CanPay but still very competitive considering that KindTap is the only one that offers credit and research indicates consumers spend more when using credit.

KindTap opened its credit product in pilot form in October 2021, and officially rolled out in February 2022. Today KindTap is integrated with over 100 merchants and growing.

Like CanPay, KindTap has customer service agents available by voice, text, or email.

SAFE Banking

We asked how the SAFE Banking might impact these providers and their competitive positions.

Dustin Eide (CanPay) indicated that the final SAFE Banking Act might only cover depository institutions, which would leave the major card networks unprotected and therefore, likely remaining on the sidelines. Eventually, cannabis will be legal and the challenges we discuss today will disappear. Dustin developed the CanPay network with the ability to integrate in conventional credit cards sometime in the future. Even so, he believes the platform could survive on its own due to the attractive cost to the merchants. With young consumers acclimated to payment platforms from Zelle to PayPal, consumers might not want to abandon a convenient cannabis payment platform for their credit cards, but only time will tell.

Cathy (KindTap) believes the SAFE Banking Act will increase accessibility to depository accounts but won’t open the playing field to major payment networks. By the time Visa and Mastercard can enter the cannabis payment market, KindTap will have developed a sufficiently large portfolio of consumers to create an affinity card with rewards.

Finding the truth

Payment platforms are complex, with numerous players and layers and all sorts of fees for the merchant. One of our go-to experts suggested that, when interviewing a payment provider, ask the right questions and get responses by email (so you have it in writing). Among those inquiries, ask the vendor hawking payment solutions for the name of the bank they are selling transaction services for and confirm the vendor is a registered ISO with that institution. Do not accept an answer like, Oh, there are so many, I can’t name them all. You want to know their main banking affiliate.

Next, confirm they are reporting the transactions to the bank as cannabis related. The vendors will generally respond in the affirmative. Ask for a letter on the bank’s letterhead addressed to the vendor confirming the bank is aware they are processing cannabis transactions, and the bank has disclosed their cannabis processing to the bank’s regulator. That is the first big test. A reputable vendor and financial institution will provide such a letter. Someone playing games or disguising the transaction will slickly talk their way around it.

Banking is a very highly and tightly regulated industry. There is no, Well, they know what we’re doing but they quietly look away because they like the volume. Ask what merchant code they use for the transactions and then look up that code here. If the code doesn’t match the product, there could be deception and fraud. If there is no merchant code, ask about the process for submitting a transaction.

Takeaways

Visiting a cannabis store? With the KindTap and CanPay apps, you can leave your wallet behind (but bring your ID to prove you are at least 21).

Do you sell to consumers? Avoid the next wave of shutdowns and get yourself a compliant payment platform.

I write about the cannabis industry, but I am also involved in a few cannabis projects. One is Stone’s Throw Cannabis, a majority social-equity owned cannabis retail store that we hope will be open by mid-2023. The store is in downtown Boston, just across the street from South Station, the busiest commuter hub in all of New England; 85,000 travelers a day pass through South Station, and we’re 125 ft. from the entry to the bus terminal, 300 ft. from the entry to the train platform, and less than 200 ft. away from a new 51-story tower being constructed above the rail lines. That tower will have 156 luxury condos, 200 hotel rooms, and 756,000 SF of office space (I know all these figures by heart; if you are raising capital, you should fully understand your competitive advantage and commit it to memory). At present, it appears we will open under the name Firebrand Cannabis.

We need a payment platform, and, in part, that is what drove my deep dive into this subject.

After evading law enforcement for nearly 13 years, an accused linked to a large-scale pharmaceutical fraud case has been arrested by Delhi Police from Surat, Gujarat. The suspect is alleged to have orchestrated a series of financial scams involving fake identities, forged documents, and dishonoured cheques used to procure high-value pharmaceutical raw materials.

Authorities say the accused, identified as Himmat Singh Lodha, is believed to have defrauded multiple pharmaceutical companies in Delhi of goods worth approximately ₹98 lakh before disappearing and remaining underground for years.

Fake Business Deals and Dishonoured Cheques Used in Fraud

Investigators claim the accused posed as a legitimate pharmaceutical trader and placed bulk orders for expensive drug ingredients, offering post-dated cheques as payment security.

In one documented case from 2013, he allegedly obtained around 550 kilograms of Gliclazide, a diabetes-related pharmaceutical ingredient, valued at over ₹26 lakh. When suppliers attempted to encash the cheques, they were reportedly returned with the remark “account closed.”

Following the transaction, the accused allegedly vacated his office and rented residence and disappeared without settling payments. He was later declared a proclaimed offender in 2016 after repeatedly failing to appear before court proceedings. Authorities had also issued a reward for information leading to his arrest.

Multiple Identities and Repeated Fraud Pattern

Police investigations further link the accused to another cheating case dating back to 2012, where he allegedly used a fake identity, “Kailash Jain,” to obtain a large consignment of Ambroxol HCL, a pharmaceutical compound used in cough medications. The value of that consignment was estimated at around ₹72 lakh.

Officials believe the accused followed a consistent modus operandi—posing as a credible businessman, securing high-value goods on deferred payment terms, and then disappearing after delivery while shutting down business operations.

Investigators suspect that forged business records, fake company credentials, and fabricated financial histories were used to build trust with suppliers and gain access to expensive raw materials.

Multi-State Surveillance Leads to Arrest in Surat

A special Crime Branch team tracked the accused through coordinated surveillance efforts across multiple cities, including Mumbai, Ahmedabad, and Surat. After nearly a month of technical monitoring and intelligence gathering, officials located and arrested him from a residential area in Surat.

Authorities also revealed that the accused had been involved in property-related activities while staying under the radar to avoid detection.

Growing Threat of Corporate Identity Fraud

The case highlights a rising trend of organised financial fraud targeting industries that rely heavily on trust-based transactions and deferred payments. Experts note that criminals increasingly exploit gaps in corporate verification systems by using fake GST registrations, temporary offices, and forged documentation to appear legitimate.

Cybercrime and financial fraud specialists warn that such schemes are becoming more complex with the widespread availability of digital business tools, making it easier to create convincing but fraudulent corporate identities.

Experts Urge Stronger Due Diligence in High-Value Transactions

Experts, including former IPS officer and cybercrime specialist Prof. Triveni Singh, emphasize the need for stricter verification procedures in commercial dealings. He noted that relying solely on paperwork or digital business profiles can expose companies to significant financial risk.

Authorities and industry experts recommend physical verification of business operations, bank account validation, and detailed background checks before engaging in high-value or deferred-payment transactions—particularly in sectors like pharmaceuticals, where single consignments can involve transactions worth crores.

Business

EU Pressure Builds on Google as Regulators Face Calls for Massive Fine Over Search Practices

A growing coalition of European industry groups is intensifying pressure on regulators to take decisive action against Google over allegations of unfair search practices that could reshape competition rules across the region’s digital economy.

Investigation Under Digital Markets Act Gains Momentum

The case is being examined by the European Commission under the European Union’s landmark Digital Markets Act (DMA), introduced to curb the dominance of major technology platforms and ensure fair competition.

Launched in March 2024, the investigation focuses on whether Google has been prioritising its own services in search results, potentially disadvantaging rival businesses that rely on online visibility to reach customers.

Industry Groups Demand Swift Action

Several prominent European organizations have jointly urged regulators to conclude the probe without further delay. They argue that prolonged investigations allow alleged anti-competitive practices to continue, putting European companies—especially startups—at a disadvantage.

Signatories include the European Publishers Council, the European Magazine Media Association, the European Tech Alliance, and EU Travel Tech.

In a joint statement, these groups warned that delays in enforcement are affecting innovation, profitability, and growth prospects for regional businesses competing in digital markets.

Google Denies Allegations

Google has rejected claims of bias, stating that its search algorithms are designed to deliver the most relevant and useful results to users. The company has also proposed adjustments to address regulatory concerns.

However, critics argue that these changes are insufficient and fail to address the core issue of market dominance.

Potential Billion-Euro Penalties

If found in violation of the DMA, Google could face significant financial penalties. Under EU rules, fines can reach a substantial percentage of a company’s global turnover, potentially amounting to billions of euros.

Regulators may also impose corrective measures requiring changes to business practices, which could have long-term implications for how digital platforms operate in Europe.

Wider Implications for Big Tech

The case highlights ongoing tensions between European regulators and major U.S. technology firms. In recent years, the EU has taken a more aggressive stance in enforcing competition laws, aiming to create a level playing field for local businesses.

A final ruling against Google could set a major precedent, influencing future enforcement actions and shaping the regulatory landscape for global tech companies operating within Europe.

As scrutiny intensifies, the outcome of the investigation is expected to play a critical role in defining the future of digital competition across the European Union.

AI & Technology

Amazon Faces Potential Criminal Trial in Italy Over €1.2 Billion Tax Evasion Allegations

Milan: U.S. tech giant Amazon is facing the prospect of a major legal showdown in Italy, after prosecutors in Milan formally requested a court to move forward with criminal proceedings over alleged tax evasion totaling approximately ₹12,500 crore (€1.2 billion).

The case targets Amazon’s European division along with four senior executives, marking one of the most significant tax-related investigations involving a global e-commerce platform in Europe.

Trial Push Despite Multi-Million Euro Settlement

The move comes even after Amazon reached a financial settlement with Italian tax authorities in December, agreeing to pay around ₹5,500 crore (€527 million), including interest, to resolve part of the dispute.

Typically, such settlements lead to the closure of criminal investigations. However, Milan prosecutors have opted to proceed, signaling a tougher stance on alleged corporate tax violations.

A preliminary hearing is expected in the coming months, where a judge will decide whether to formally indict the company and its executives or dismiss the case.

Allegations of VAT Evasion Through Marketplace Sellers

At the center of the investigation are claims that Amazon’s platform enabled non-European Union sellers to avoid paying value-added tax (VAT) on goods sold to Italian consumers between 2019 and 2021.

Prosecutors allege that the company’s marketplace structure allowed thousands of foreign vendors—many reportedly based in China—to operate without fully disclosing their identities or tax obligations. This, authorities argue, led to substantial VAT losses for the Italian government.

Under Italian law, online platforms facilitating sales can be held partially liable if third-party sellers fail to comply with tax requirements, a key point in the prosecution’s case.

Italian Government Named as Affected Party

In their filing, prosecutors identified Italy’s Economy Ministry as the injured party, citing significant financial damage resulting from the alleged tax evasion.

Legal experts say the outcome of the case could have wide-ranging implications across the European Union, where VAT systems are harmonized and similar compliance rules apply to digital marketplaces.

Multiple Investigations Add to Pressure

The VAT probe is just one of several legal challenges facing Amazon in Italy. The European Public Prosecutor’s Office is reportedly examining additional tax-related issues covering more recent years.

Meanwhile, Milan authorities are pursuing separate investigations into alleged customs fraud linked to imports from China and whether Amazon maintained an undeclared “permanent establishment” in Italy—potentially exposing it to higher tax liabilities.

In a separate regulatory action, Italy’s data protection authority recently ordered an Amazon unit to stop using personal data from over 1,800 employees at a warehouse near Rome.

Amazon Denies Allegations

Amazon has consistently denied wrongdoing and indicated it will strongly contest the allegations in court if the case proceeds. The company has also warned that prolonged legal uncertainty could impact investor confidence and Italy’s appeal as a destination for international business.

Broader Impact on Europe’s Digital Economy

If the case moves to trial, it could become a landmark moment for the regulation of global e-commerce platforms in Europe. Governments across the region are increasingly scrutinizing how digital marketplaces handle tax compliance, especially in cross-border transactions.

With online retail continuing to expand, regulators are under mounting pressure to ensure that multinational platforms and third-party sellers adhere to the same tax rules as traditional businesses.

-

Business3 years ago

Business3 years agoPot Odor Does Not Justify Probable Cause for Vehicle Searches, Minnesota Court Affirms

-

Business3 years ago

Business3 years agoNew Mexico cannabis operator fined, loses license for alleged BioTrack fraud

-

Business3 years ago

Business3 years agoAlabama to make another attempt Dec. 1 to award medical cannabis licenses

-

Business3 years ago

Business3 years agoWashington State Pays Out $9.4 Million in Refunds Relating to Drug Convictions

-

Business3 years ago

Business3 years agoMarijuana companies suing US attorney general in federal prohibition challenge

-

Business3 years ago

Business3 years agoLegal Marijuana Handed A Nothing Burger From NY State

-

Business3 years ago

Business3 years agoCan Cannabis Help Seasonal Depression

-

Blogs3 years ago

Blogs3 years agoCannabis Art Is Flourishing On Etsy